How resilient is the insurance industry against climate change?

New research has found there are several steps insurers can take to improve the way they assess and manage the impacts of climate change on the community

The escalating frequency and severity of extreme weather-related events have shone a brighter regulatory spotlight on insurance risk and climate change, and all eyes in the insurance industry are on Australia as it enters its summer season this year. The Bushfire and Natural Hazards Cooperative Research Centre is forecasting above-normal fire conditions for parts of Australia this summer. Last year, record-breaking temperatures and months of severe drought fuelled a series of massive bushfires across Australia. More than 11 million hectares were devastated, and insured losses were estimated at up to A$1.9 billion.

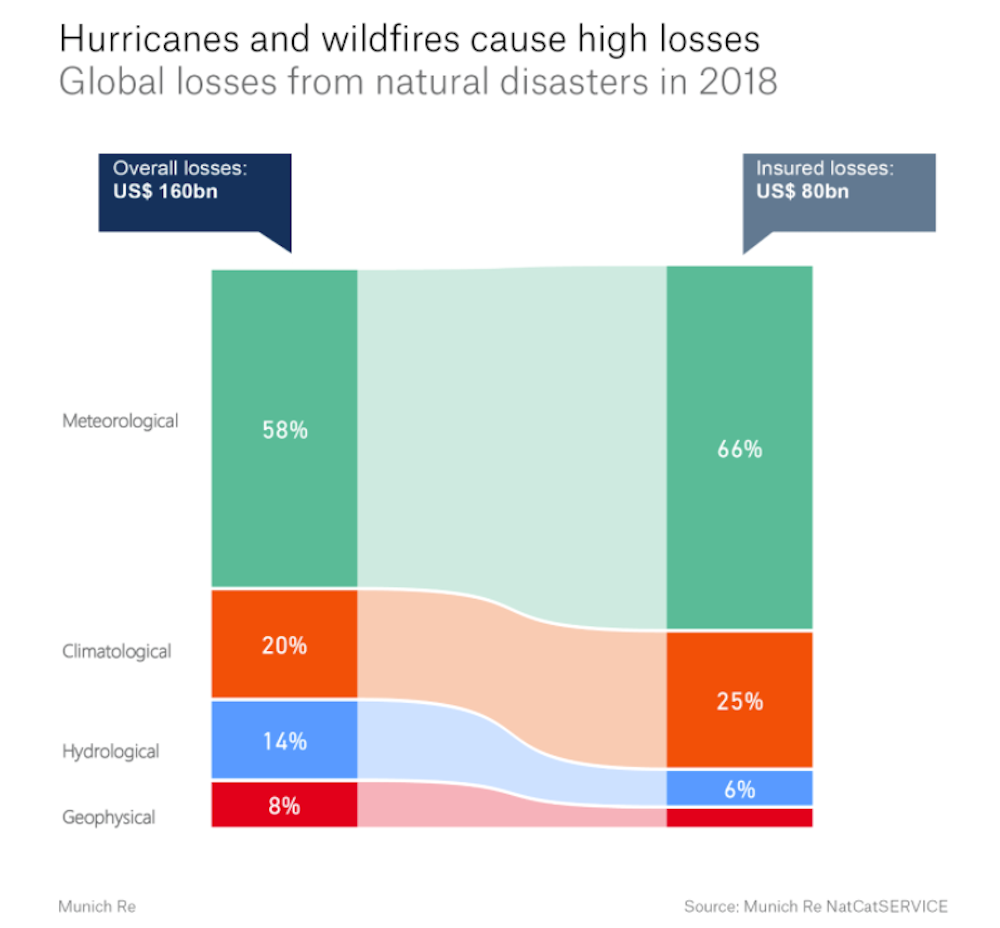

In 2018, natural disasters killed more than 10,000 people and left millions more homeless. In the same year, natural catastrophe-related economic losses reached US$160 billion (A$215 billion) (half of which were all insured losses). The vast majority – 95 per cent – of the registered events were weather-related.

So insurers are recognising that the mid- to long-term outlook on climate change carries some massive risks. With Australia at the centre of a geographic region adversely affected by climate change, it is imperative for the insurance industry to assess and manage the adverse impacts of extreme weather to ensure Australia’s climate resilience.

Understanding the risks posed by climate change

The Insurance Council of Australia states that climate change is a shared risk and a shared responsibility, and one which presents several challenges for the insurance industry and community, such as:

- Changing physical risk, extreme weather patterns, and the need for new tools, modelling, and investment to inform decision making, climate adaptation and mitigation,

- The continued need for suitable and affordable insurance products to protect the community and businesses against perils,

- A changing economy and the transition to a low carbon emissions economy, and

- The need to ensure the solvency and stability of prudentially regulated entities.

So what does the insurance industry need to do to become more resilient against climate change and to protect people from potentially devastating financial and human losses? A new study based in the US offers some insights.

Facing the heat: climate change and mortality

The paper, Joint Extremes in Temperature and Mortality: A Bivariate POT Approach, examines insurance risk management by jointly modelling extreme climate risk and extreme mortality risk. Climate change directly impacts the insurance sector, since catastrophic weather events and mortality experience can simultaneously trigger large losses across different lines of the insurance business, according to Professor Qihe Tang, Director of Research in the School of Risk & Actuarial at UNSW Business School, and his co-author Dr Han Li, Senior Lecturer in the Department of Actuarial Studies and Business Analytics at Macquarie Business School.

Their study is amongst the first to explore the unique relationship between extreme climate and extreme mortality from an actuarial perspective, and their approach can be easily adapted for future research on related topics such as the impact of climate change on health insurance. A key challenge in modelling extreme risks is the scarcity of observations.

Fortunately, extreme value theory (EVT) can be used to provide results beyond observed values. To model the extreme dependence between temperature and mortality, the authors employed a cutting-edge bivariate “peaks over threshold” (POT) approach. "As a simplified example, if we know a higher than usual temperature on a day, the bivariate POT allows us to estimate the likelihood of a higher than usual number of deaths that day. The study quantifies the extreme dependence between death counts and temperature indexes for different age groups and across different geographical regions in the US," the authors explain.

In the paper, the authors note the World Health Organization (WHO) is expecting 250,000 additional deaths annually between 2030 to 2050 due to climate change-induced intense temperature fluctuations and climate-sensitive diseases. One of the aims of their research is to produce broader impacts on society, in promoting climate resilience in the insurance sector, as well as in protecting vulnerable segments of the population.

“Our age-region-specific analysis of joint extremes in temperature and mortality shows that the levels of exposure and resilience to extreme weather vary across different geographical regions and age groups. We also find that the frequency of extremely low temperatures has a stronger impact on mortality, especially for older ages,” say the authors.

Practical steps

In Australia, climate extremes are only becoming more frequent – recent examples include September 2019 as one of the driest Springs on record, and January 2020 was the third warmest January in history. NSW also experienced its hottest November weekend on record.

In the paper, the authors write that climate change has become one of the top risks that pose a serious threat to global health and human lives, so in the life insurance context, effective management and mitigation of climate risk are increasingly important for solvency considerations, as weather-driven hazards can lead to an unanticipated adverse claim experience.

Looking ahead, better risk awareness from the life insurance industry, as well as innovative risk mitigation tools such as mortality catastrophe (CAT) bonds can help to build a more sustainable insurance sector and economy, and ultimately a more climate-resilient society.

So what practical steps can the insurance industry implement? Firstly, the industry needs better risk awareness. “Climate-related research is in urgent demand to better understand the implications of climate change for insurance industries. In the enterprise risk management framework, we need to first identify and understand the risk, and then quantify and mitigate the risk,” the paper says.

Second, the industry should incorporate environmental factors in insurance pricing. “Besides traditional insurance pricing factors, scenario-based analysis should be considered to project future claim experience under different climate conditions,” say the authors.

Finally, insurance-linked securities (ILS) offer a risk mitigation solution. For example, mortality catastrophe (CAT) bonds have been used as a risk mitigation tool by many large reinsurance companies – such as AIG, Axa and Allianz – to transfer extreme mortality risk to the capital market. Such a solution can go a long way to promote resilience in the industry, and in turn, its ability to manage the risks posed by climate change.

This paper has been accepted for publication at the North American Actuarial Journal and is awaiting publication. The most recent version of the paper can be downloaded here. For more information, please contact Professor Qihe Tang, Director of Research in the School of Risk & Actuarial at UNSW Business School directly.